Are you wondering who might benefit from Affordable Care Act (ACA) plans when selling or marketing insurance plans to clients? We’ve got your answer.

Explore who makes an ideal client in different situations of clientele eligibility below.

What Is an ACA Plan?

To identify an ideal potential ACA client, it’s important to first understand what an ACA plan is. The ACA expanded health care options to millions of Americans when it was signed into law in 2010 by former President Obama, leading to the creation of the nickname “Obamacare.”

An ACA plan is one that meets the legal requirements set forth by the Affordable Care Act. Some of those requirements are:

- Covers Essential Health Benefits

- Offers preventative services at no cost

- Doesn’t deny coverage based on pre-existing conditions

- Has no lifetime or annual limits

ACA coverage can be bought from federal or state health exchanges or directly from carriers, off the exchange. Insurance agents can help their clients enroll in these plans if the carrier allows agent sales assistance.

An ACA plan is one that meets the legal requirements set forth by the Affordable Care Act.

Open enrollment for these plans runs from November 1 to January 15 of each year. Many clients will qualify for subsidies that help lower the costs of health insurance for households closer to the federal poverty level (FPL).

Who Qualifies for ACA Health Insurance?

There are a few basic eligibility criteria for ACA plans interested clients must meet. To be eligibile to enroll in marketplace coverage, an individual must:

- Live in the United States

- Be a U.S. citizen or national, or be a lawfully present non-citizen in the U.S.

- Not be incarcerated

- Not be enrolled in other Minimum Essential Coverage (MEC), such as Medicare or Medicaid

All clients have different needs, so finding the right ACA insurance plan for your potential clients is critical.

Someone can typically make changes to their ACA coverage during the Open Enrollment Period (OEP), which runs November 1 to January 15 each year on the federal exchange. State exchanges may offer OEPs that run through different dates. There may even be a qualifying event that triggers a Special Enrollment Period (SEP), so be sure to ask your clients as many questions as possible about their specific circumstances to determine if they qualify to enroll in or make changes to existing ACA coverage outside of Open Enrollment.

What Kind of Clients Would Benefit From ACA Health Plans?

Who are the clients you should focus on when selling ACA plans to eligible beneficiaries? There are many reasons why someone may best be covered by a marketplace plan. Let’s explore five types of clients that are ideal for ACA plans.

1. A Worker Whose Employer Does Not Provide Affordable Insurance

Sometimes, employees are in positions where they have one or more jobs where their employers don’t provide insurance. Most part-time positions don’t offer insurance simply because the employers are not required by law to do so. This opens a large clientele pool due to the number of part-time workers in the U.S. alone — about 28,523 workers.

Even if an employer offers coverage to its employees, if it is deemed unaffordable, an employee is eligible to enroll in a marketplace plan with access to subsidies.

ACA insurance can be a great option for employees without access to affordable employer group coverage.

ACA insurance can be a great option for employees without access to affordable employer group coverage. Through the marketplace, you could offer them an affordable way to acquire and maintain health coverage.

Note: Prior to PY 2023, the affordability calculation for an employer group plan was based on the cost of employee-only coverage. If coverage was deemed affordable for the employee but not for family coverage, the family was still ineligible for premium tax credits on the marketplace. This was known as the “family glitch.”

Following the resolution in 2022 for PY 2023, there’s now a separate affordability determination for the employee (based on employee-only coverage) and the employee’s dependents (based on the total cost of family coverage). If the employer subsidizes most of the cost for employee-only coverage but not family coverage, the employee’s coverage is deemed affordable and they are not eligible for premium tax credits. They would enroll in the group plan. Because coverage for the family is deemed unaffordable, the family could enroll in a marketplace plan and be eligible for premium tax credits.

2. Startup or Solo-Run Businesses

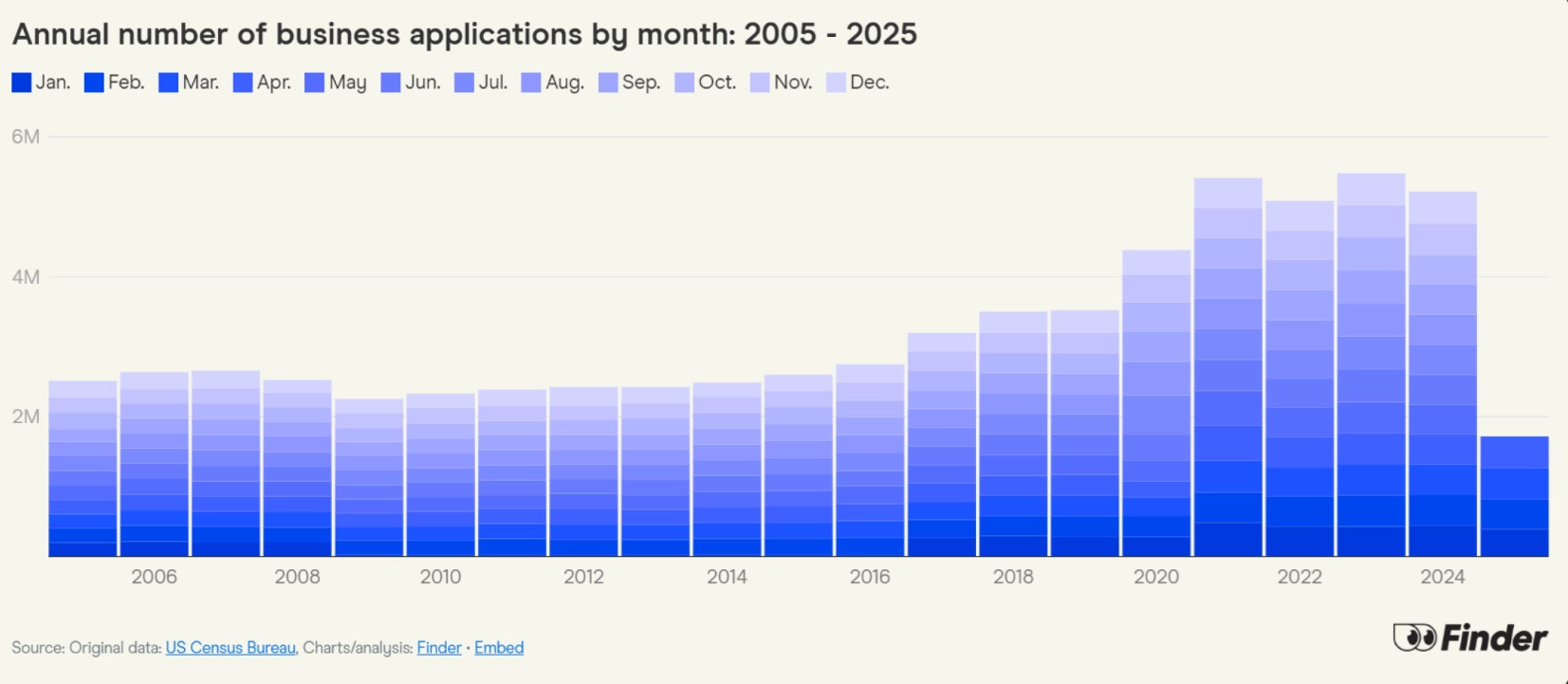

When starting a business, offering insurance or even acquiring insurance for themselves as a business owner can be difficult. This is especially true for those flying solo. According to the U.S. Department of the Treasury, approximately 430,000 new business applications are filed each month. These individuals could be future clients who could be looking for an affordable health care option through the marketplace!

New businesses open all the time, growing vastly higher since 2020. In 2024 alone, approximately 5.21 million applications were lodged. The number of businesses goes into the millions, giving an expansive array of different clients that could be looking into an ACA plan.

3. Freelancers or Self-Employed Workers

The number of freelance workers has skyrocketed post-COVID. Approximately 36 percent of the entire U.S. workforce is now working in a freelance position! There were about 59.7 million freelance workers in 2018 and that number has jumped up by 20 million people since then! Many freelance workers do not have insurance offered to them via an employer. Acquiring coverage as a self-employed individual can be more difficult and expensive. You can help make it easier by letting these individuals know ACA coverage can be a great option!

Freelance work is known to be rather unstable when it comes to income, especially because the income is never guaranteed. Affording insurance in any way can be trying because of that. Typically, an ACA plan without premium tax credits will cost around $483 for a 30-year-old in 2025. However, available premium tax credits can help offset the cost of the insurance provided. In 2024, 92 percent of shoppers qualified for subsidies, and 75 percent were able to find coverage for less than $10 a month per the Centers for Medicare & Medicaid Services (CMS). Enhanced subsidies allow individuals with household incomes above 400 percent of the federal poverty level to qualify for subsidies through the end of 2025. Household incomes between 100 and 400% of the federal poverty level have access to higher subsidies.

4. Recently Terminated or Resigned Employees

Loss of employer group coverage triggers an SEP for marketplace coverage.

ACA plans can step in the moment employment agreements are severed.

ACA plans can step in the moment employment agreements are severed. While there are options like COBRA, if an individual voluntarily gave up their COBRA benefits or never enrolled in their employer’s health plan, they wouldn’t qualify. According to the United States Department of Labor, there are about 7.1 million unemployed Americans in 2025, giving a wide and diverse number of clients who might be a good fit for an ACA plan.

5. Early Retirees Who Don’t Qualify for Medicare

Early retirement can occur because of numerous factors, such as job loss or simply wanting to retire early. In some instances, if a retiree isn’t at least 65 years old, they will not qualify for Medicare. In 2024 alone, more than 50 percent of all retirees had to retire early due to unforeseen circumstances. This could leave them without an insurance plan that they may need.

We hope that exploring some of the best clientele for ACA insurance plans will help you acquire new business and grow your client base. Now that we’ve explored some of the most ideal clients for under-65 insurance options here, it’s your chance to make those connections in your community that can lead to additional sales!

For more helpful tools and resources, make sure you’re registered with Ritter to help you even further on your independent insurance agent journey!

Not affiliated with or endorsed by Medicare or any government agency.

Share Post